The Investment Was Working. The Reporting Was Not.

The investor had three good-looking private deals.

One was a logistics business in Southeast Asia.

One was a processing facility in West Africa.

One was a real estate project in Eastern Europe.

Money was coming in, although not every month.

The assets were still operating.

Nothing obvious had gone wrong.

Then the bank asked a simple question:

“What exactly do you own, what is it worth, and what cash has it produced?”

The investor had documents.

But the documents did not tell one clear story.

Some reports were in local currency.

Some were in dollars.

Some arrived monthly.

Others arrived late, or not at all.

The bank did not say the assets had failed.

It said the portfolio was hard to understand.

That is a different problem.

But it can still cost you money.

In private markets, especially in less standardized markets, poor reporting can make a good asset look risky.

Why Clear Reporting Matters More Outside Major Financial Centers

In large public markets, information is usually easier to compare.

Listed companies often report under IFRS or local accounting rules.

IFRS is a global accounting language used to make financial statements more comparable across countries.

There are also stronger expectations around audits, disclosure, board oversight, and investor information.

The OECD’s 2023 corporate governance principles describe disclosure and transparency as central to investor protection and capital market confidence.

Private deals are different.

A private credit deal, minority stake, or development project may not report like a listed company.

The information can be late, incomplete, or prepared in different formats.

That does not always mean something is wrong.

But it does mean the investor needs a system.

Think of it like owning several rental properties in different countries.

One manager sends you rent reports in naira.

Another sends expenses in baht.

Another sends updates only when asked.

You may still be making money.

But if your lender, spouse, heir, or advisor asks for a full picture, you may struggle.

That struggle reduces your financial flexibility.

Banks dislike unclear information.

Buyers discount unclear assets.

Families fight over unclear ownership records.

The asset may be valuable.

But without clean reporting, the value becomes harder to defend.

This is where the Family Office Lite idea matters.

A Family Office Lite system is a simple version of family office discipline.

It helps serious investors track deals, documents, cash flow, risk, and reporting without building a full institution.

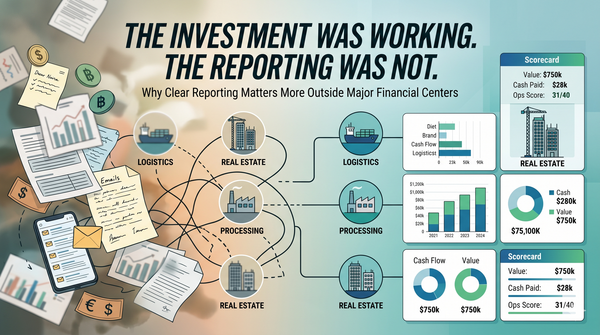

What This Looks Like With Real Numbers

Imagine you have $750,000 spread across three private investments.

You invested $250,000 in a logistics company.

You invested $300,000 in a food processing facility.

You invested $200,000 in a real estate development.

On paper, everything looks fine.

The logistics company has paid $28,000 in distributions.

The processing facility says revenue is growing.

The real estate project says the site value has increased.

Now your bank asks for five things:

What is the current value of each asset?

How much cash has each asset paid back?

What currency is each asset exposed to?

Are any promises in the loan documents being breached?

Can you prove your legal rights?

These are not academic questions.

If you cannot answer them quickly, the bank may treat your portfolio as riskier.

That can mean lower borrowing capacity, stricter terms, or slower approval.

The same issue appears during exits.

A buyer may like your investment.

But if the records are messy, the buyer may ask for a discount.

The discount is not always about the business.

Sometimes, it is about the uncertainty.

That is the hidden cost of weak reporting.

What Can Go Wrong

Clean reporting does not remove investment risk.

A bad deal can still lose money.

A currency can still fall.

A partner can still behave badly.

A project can still miss its deadlines.

The real benefit is different.

Good reporting helps you see problems earlier.

It also helps you defend your position when someone questions the asset.

There are practical risks.

Operators may resist monthly reporting.

Different countries may use different accounting rules.

Currency movements can make performance look better or worse than it is.

Private markets also tend to be less transparent than public markets.

IOSCO warned in 2023 that private finance can carry lower transparency and weaker access to information for some investors.

Manual reporting can also become tiring.

That is why the system must be simple.

A reporting system that nobody uses is not a system.

It is decoration.

The goal is not perfection.

The goal is consistency.

Build a Monthly Close for Your Private Portfolio

A monthly close means you review and organize your investment information every month.

Here is the Family Office Lite version.

First, create one standard reporting template.

Ask every operator or counterparty to send the same core items:

Monthly income statement

Cash received and cash spent

Debt balance, if any

Current valuation estimate

Key performance numbers

Any missed payment or covenant issue

A covenant is a promise in a loan or investment agreement.

For example, the borrower may promise to maintain insurance or send reports monthly.

Second, convert everything into two currencies.

Track each deal in its local currency.

Then also show it in your main reporting currency, such as dollars, euros, or pounds.

This helps you separate business performance from currency movement.

Third, build one master dashboard.

It should show:

Capital invested

Current carrying value

Cash received

Estimated return

Currency exposure

Covenant status

Next reporting date

Missing documents

Fourth, keep a covenant and trigger register.

This is a simple list of every promise, deadline, insurance requirement, and reporting obligation.

No covenant should depend on memory.

Fifth, store documents properly.

Keep signed agreements, amendments, reports, breach notices, valuation notes, and key emails in one organized folder.

Use dates.

Use version control.

Use clear file names.

Sixth, review the portfolio every quarter.

Ask four questions:

Has the risk changed?

Has the operator’s behavior changed?

Has currency exposure changed?

Can the asset still be refinanced, sold, or transferred?

Finally, score your portfolio.

Use this simple FO-Lite Ops Readiness Scorecard.

Score each area from 0 to 5:

Reporting and controls

Documentation survivability

Deal monitoring

Banking durability

Counterparty and enforcement map

Currency tracking

Covenant tracking

Exit readiness

Total score:

0 to 12: Your yield is fragile.

13 to 26: The portfolio is operationally investable.

27 to 40: The portfolio is more bankable and transferable.

The goal is not to impress anyone with reports.

The goal is to make your money easier to understand, defend, finance, sell, and pass on.

“Opacity increases the risk premium. Clarity increases leverage.”

Global Wealth Diagnostic

The Global Wealth Diagnostic is a fast, personalized diagnosis that helps high earners identify the smartest next steps for building wealth across borders. It evaluates your current position, highlights your biggest opportunities and gaps, and gives you a practical roadmap for investing, structuring, and moving with more confidence.

Sources

Original contributor draft supplied to I-Invest.

IFRS Foundation, “Who uses IFRS Accounting Standards?”, accessed April 2026.

OECD, “G20/OECD Principles of Corporate Governance 2023,” published 2023.

IOSCO, “Thematic Analysis: Emerging Risks in Private Finance,” published September 2023.

World Bank Enterprise Surveys, financial statement and audit survey materials, updated 2025 and 2026.

IFC, ESG Guidebook and investment governance materials, published 2021.

Disclosure

This article is general information, not personal investment, tax, or legal advice. It reflects conditions and data available as of April 2026. I-Invest Magazine and the author do not receive compensation from entities mentioned unless explicitly stated. Readers should obtain independent professional advice before taking action.