The problem is not coffee. It is credibility

Coffee can be a commodity, a cultural product, and an operating business at the same time. That combination attracts capital, but it also attracts scrutiny.

Tax authorities do not audit “coffee” or “collecting” in the abstract. They audit the story the records tell.

When that story shows repeated losses, informal bookkeeping, mixed personal and business spending, weak contracts, inconsistent inventory values, or private lifestyle benefits embedded in the activity, the question becomes predictable: is this a genuine profit-seeking enterprise, or a personal pursuit wrapped in business language?

For globally mobile founders, HNW individuals, and family offices, that distinction matters beyond tax efficiency. A weak business posture can lead to disallowed deductions, recharacterized expenses, penalties, prolonged disputes, banking friction, and valuation problems in financings, exits, or estate planning.

The aim is not to force a preferred classification. The aim is to build an operating posture that can survive scrutiny.

What this is, and who it is for

This is a credibility framework for operators, allocators, and advisors assessing coffee and origin-linked agricultural businesses. It is especially relevant where personal passion, family capital, and informal operating habits risk colliding with tax, banking, or diligence standards.

What “hobby business” means in practice

Different jurisdictions use different tests, but the core question is similar: does the activity show real profit intent and commercial behavior?

In the United States, Internal Revenue Code Section 183 limits deductions for activities not engaged in for profit. The current code also includes a rebuttable presumption in the taxpayer’s favor if gross income exceeds deductions in three out of five consecutive taxable years. Treasury Regulation § 1.183-2(b), as referenced by the IRS, and current IRS guidance both emphasize that no single factor controls and that objective evidence matters, including complete books and records and whether losses reflect start-up conditions or circumstances outside the operator’s control.

In the United Kingdom, HMRC’s “badges of trade” framework looks at indicators such as profit-seeking motive, number of transactions, nature of the asset, source of finance, interval between purchase and sale, and the way the sale is carried out. HMRC also states that no single badge is conclusive and that the overall impression matters.

The practical translation is straightforward. Loving the product is not enough. You need records, contracts, pricing logic, and operating decisions that show commercial intent.

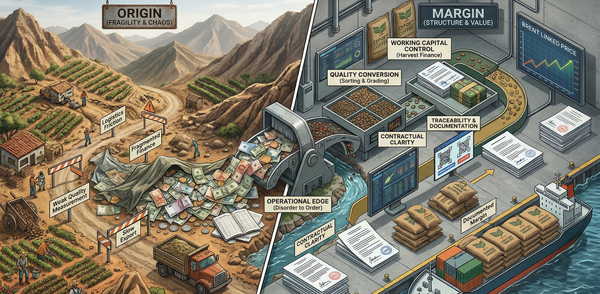

Where credibility breaks first

In coffee and agricultural exposure, scrutiny usually lands in five places first.

Recordkeeping and separation. Can the business show separate accounts, clean bookkeeping, and a consistent chart of accounts? Or do personal and business expenses move through the same channels?

Pricing and contracts. Can the operator explain how lots, services, or products are priced? Are quality specifications, delivery terms, title transfer, payment dates, and dispute mechanisms documented consistently?

Inventory and valuation discipline. Coffee is a physical commodity. Quality shifts, shrink, spoilage, and grading differences affect value. Loose inventory methods weaken tax positions and undermine lender confidence.

Governance and decision-making. Are there approval controls, related-party transaction records, and clear signatory authority? Or does everything depend on one person’s informal judgment?

Commercial realism. Does the operating plan respond to market conditions? Are margins tracked, pricing adjusted, and unprofitable lines cut? Or do losses repeat while private benefits accumulate?

A credible coffee business does not rely on story alone. It shows an operating model that can be inspected.

Revenue is enforceable. Revenue quality begins with contracts. At minimum, contracts should define the lot, traceability standard, acceptance process, pricing method, delivery terms, transfer of title and risk, payment terms, remedies, and compliance representations.

Working capital is controlled. In origin and trade, working capital is often the business model. Cash handling, supplier onboarding, reconciliations, approval controls, and documented advances matter as much as top-line growth. Cash movement without controls is a warning sign for both authorities and banks.

Traceability doubles as evidence. Traceability is not only an ethical or branding issue. It is also documentary proof. The OECD-FAO Guidance for Responsible Agricultural Supply Chains sets out a five-step, risk-based due diligence framework to identify, assess, mitigate, and account for adverse impacts across agricultural supply chains. Even where a strategy is not positioned as impact-led, due diligence and traceability strengthen documentation, reduce disputes, and improve bankability.

Profit motive shows up in operating behavior. A credible profit objective is visible in decisions, not slogans. Budgets, variance tracking, price resets, supplier renegotiation, product-line exits, and margin improvement plans all help show that management is trying to make the business economically viable. In the United States, the IRS explicitly includes businesslike records, expertise, time and effort, profit history, and whether losses reflect start-up conditions or events outside the operator’s control among the relevant factors.

Key numbers and assumptions

Before scaling, the operator should be able to produce a basic institutional file covering gross margin by lot or customer, inventory days and shrink assumptions, customer concentration, DSO and DPO, cash conversion cycle, FX exposures by currency, related-party balances, and break-even by harvest cycle or operating season.

If those numbers are unavailable, the business is not ready for institutional capital, and its tax posture is harder to defend.

Institutional capital reality check

Any serious underwriting exercise should answer five questions clearly.

Where does the cash come from? Founder capital, family capital, supplier credit, warehouse finance, and trade finance do not carry the same governance expectations.

In what currency? A business that buys in local currency, carries inventory, and sells in dollars or sterling is not just managing margin. It is also managing FX exposure and timing risk.

Under what legal setup? Holding companies, operating entities, SPVs, and related-party funding lines should match the commercial reality and the reporting story shown to banks, tax authorities, and counterparties.

What is the plausible return range? The return case should be tied to unit economics, working-capital cycle, default assumptions, shrink, logistics risk, and FX friction. A projected return that ignores those variables is not underwriting. It is aspiration.

What can go wrong? Crop shortfalls, counterparty default, delayed export documents, quality claims, sanctions issues, and governance failure all need a visible downside case.

Global Wealth Diagnostic

The Global Wealth Diagnostic is a fast, personalized assessment that helps high earners identify the smartest next steps for building wealth across borders. It evaluates your current position, highlights your biggest opportunities and gaps, and gives you a practical roadmap for investing, structuring, and moving with more confidence.

Risks and failure paths

Even well-run operators can face scrutiny. Start-up losses, price volatility, weather events, logistics disruption, and currency moves can all pressure margins. The problem begins when those facts are not matched by records, controls, and a coherent explanation.

A good business can survive bad seasons. A weak file struggles to survive questions.

Variants and alternatives

Not every coffee-adjacent activity should be forced into a trading-business narrative. In some cases, a smaller side business with strict separation is more defensible than a platform story that cannot support its own controls. In other cases, a personal collecting or lifestyle activity may be cleaner if it is reported consistently and not dressed up as an enterprise.

The wrong structure is often more dangerous than a modest one.

Operator Readiness Scorecard

Use a 100-point review before adding leverage, outside investors, or multi-entity structuring.

Commercial posture, 0 to 20: enforceable contracts, documented pricing method, customer concentration tracking, and visible unit economics.

Controls and accounting, 0 to 20: separate accounts, reliable bookkeeping, inventory system, reconciliations, and payment audit trail.

Governance and evidence, 0 to 20: signatory matrix, decision minutes for key actions, related-party register, and documented profit-improvement actions.

Supply-chain proof, 0 to 20: lot records, supplier onboarding, logistics documents, and counterparty due diligence files.

Tax and compliance readiness, 0 to 20: documented business classification posture, valuation discipline, and a consistent reporting story across entities and banks.

A high score does not remove audit risk. It reduces ambiguity. Ambiguity is what usually turns review into damage.

Sources

United States: 26 U.S.C. § 183, “Activities not engaged in for profit,” text in effect February 17, 2025; IRS, “How do you distinguish between a business and a hobby?”, page last reviewed February 2, 2026; 26 C.F.R. § 1.183-2(b), current regulation referenced by the IRS.

United Kingdom: HMRC Business Income Manual BIM20205, “Meaning of trade: badges of trade: summary,” updated March 18, 2026.

OECD/FAO: OECD-FAO Guidance for Responsible Agricultural Supply Chains (2016), OECD Publishing.

Disclosure

This article is general information, not personal investment, tax, or legal advice. It reflects conditions and data available as of March 2026. I-Invest Magazine and the author do not receive compensation from entities mentioned unless explicitly stated. Readers should obtain independent professional advice before taking action.